IEA Report on Solar PV Global Supply Chain and Recommendations

The amount of solar PV deployed around the World has increased significantly, while cost of solar PV is continuously decreasing. Solar PV is and will continue to play a crucial role towards climate goals.

A recent report published by IEA (International Energy Agency) examines solar PV supply chain from raw materials all the way to the finished product, spanning the five main segments of the manufacturing process: polysilicon, ingots, wafers, cells and modules. The analysis covers supply, demand, production, energy consumption, emissions, employment, production costs, investment, trade and financial performance, highlighting key vulnerabilities and risks at each stage. In order to reduce the supply chain issues, diversification of supply chain steps are recommended. It also provided an overview about the steps taken by Governments to support the local solar PV manufacturing and recommendations to further support this.

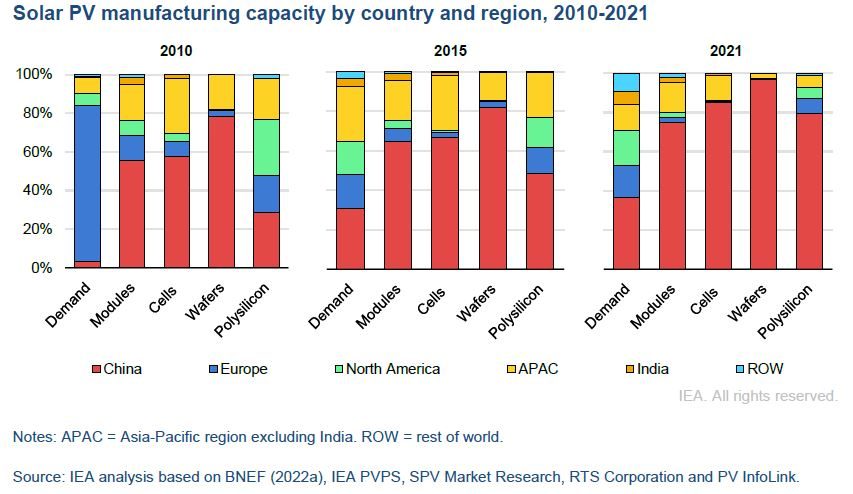

China currently dominates the global solar PV supply chains. China has developed itself a leading solar PV manufacturer by investing heavily in last decade and covers almost 80% of all the manufacturing stages of the Solar PV. China has been instrumental in brining down the Solar PV cost, but at the same time the geographical concentration in global supply chain creates some potential challenges that need to be address through diversification.

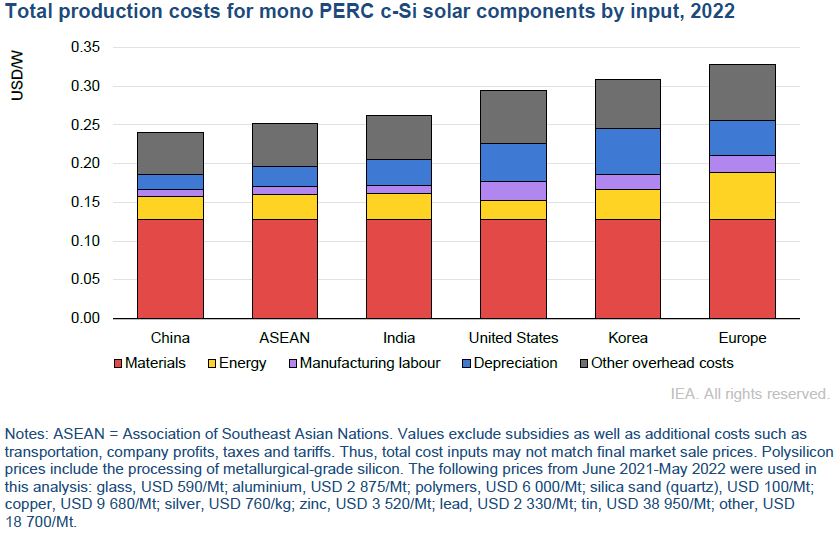

China is the most cost-competitive location to manufacture all the components of Solar PV supply chain. Costs in China are 10% lower that in India, 20% lower than in United States, and 35% lower than in Europe.

Three Important Factors to consider:

- Low-cost electricity: Electricity accounts for over 40% of production cost for polysilicon and nearly 20% of ingots and wafers. The majority of electricity used in China for polysilicon production at an average price of around USD 75 per MWh, roughly 30% below global industrial price average. Therefore, to develop competitive manufacturing requires access to comparable lower electricity price.

- Solar PV manufacturing around low-carbon industrial clusters: Solar panel manufacturers can also use their own products to generate the required electricity on site. Hence, can access to low carbon and cost competitive electricity. For new manufacturing facilities, locations near to emerging industrial clusters (e.g., renewables-based Hydrogen) could provide an additional advantage. Economies of scale can also help to bring down the cost.

- Recycling of Solar PV: Supplies from recycling could meet over 20% of solar PV industry demand for aluminum, copper, glass, silicon and almost 70% of silver between 2040 and 2050. Existing recycling process struggle to maintain sustainable operations due to recycling cost.

The IEA’s five key policy actions points

- Diversify manufacturing and raw material supplies through policies considering it as a key point towards clean energy transition.

- De-risk manufacturing through finance, tax policies and other support and research measures.

- Ensuring environmental and social sustainability through transparency and international cooperation.

- Improving solar cell efficiency by fostering innovation and research.

- Developing recycling capabilities through regulatory framework and recycling friendly design.